As the housing market steadies after a turbulent decade, many homeowners are turning to personal loans for renovation projects, debt consolidation, or unexpected expenses. Yet the numbers on the table show that borrowing costs remain stubbornly high. In this deep dive, we break down why rates are where they are, what credit scores mean for your rate, and how online lenders compare to banks and credit unions.

Where Are Rates Heading?

According to NerdWallet’s latest anonymized pre‑qualification data from 2026, the average personal loan APR for consumers with fair credit (630–689) was 17.93%. Those with good credit (690–719) averaged 14.48%, while excellent borrowers (720+) secured a respectable 11.81%. These figures are derived from users who applied through NerdWallet’s portal, giving us a realistic snapshot of what most people face.

While the numbers have dipped slightly compared to peak rates in 2021—when some borrowers faced APRs above 30%—they still sit at the upper end of the typical personal loan spectrum. The Federal Reserve’s recent policy shifts, such as the 0.25% cut on the federal funds rate in December 2025, have not yet trickled down to consumer borrowing costs because personal loans are largely interest‑rate agnostic.

In practice, this means that a borrower with a 700 credit score might still find themselves paying around 14–15% APR if they apply through an online lender. If you’re aiming for the best possible rate, you’ll need to shop aggressively across multiple platforms and consider factors beyond just your score.

Why Are Rates Still So High?

Several forces keep personal loan rates elevated:

- Economic uncertainty: Lenders hedge against inflation by tightening credit standards, pushing rates up for riskier borrowers.

- Lender competition: Banks and credit unions often undercut each other on the lower end of the market, but online lenders compete more on speed than rate, leading to higher average APRs.

- Regulatory costs: Compliance with new consumer protection rules adds overhead for lenders, which is passed onto borrowers.

In short, while you’re not paying the same sky‑high rates as in the early 2020s, the cost of borrowing remains a serious consideration for anyone planning major expenditures.

Online Lenders vs. Traditional Banks and Credit Unions

The market is split into three main categories: online lenders, commercial banks, and credit unions. Each offers distinct APR ranges, loan terms, and eligibility criteria. Below is a snapshot of the average rates for March 2026 based on NerdWallet’s reviews.

| Institution Type | APR Range (March 2026) |

|---|---|

| Online Lenders | 6.49% – 35.99% |

| Commercial Banks | 6.74% – 26.74% |

| Credit Unions | 7.89% – 18.00% |

While banks and credit unions generally offer tighter ranges, they also tend to require longer application processes and stricter documentation. Online lenders can approve in minutes, but the trade‑off is a broader spread that includes higher APRs for less‑favorable credit profiles.

Which Path Is Right For You?

If you’re a borrower with excellent credit (720+), a credit union could offer you an APR as low as 7.89%—the lowest among the three categories. However, you’ll need to be a member of the institution’s network.

For borrowers in the fair or bad credit ranges, online lenders often provide the fastest access, but expect rates closer to the high end (20–35%). Banks may offer slightly lower APRs for similar profiles, but approval can take days or weeks.

The Role of Credit Score

Credit score remains the single most influential factor in determining your loan rate. The NerdWallet table illustrates a clear trend: each 10‑point jump above 720 yields an approximate 1–2% reduction in APR.

- Excellent (720+): 11.81% average

- Good (690–719): 14.48% average

- Fair (630–689): 17.93% average

- Bad (<630): 21.65% average

Beyond the score, lenders scrutinize income, debt‑to‑income ratio, and payment history. A high monthly take‑home pay can offset a lower credit score, while a low DTI (ideally <50%) signals stability.

Improving Your Rate With Co‑Signers

Borrowers with fair or bad credit often turn to co‑signers or joint applicants. A partner with excellent credit and higher income can lower the lender’s perceived risk, potentially slashing your APR by 1–2%. This strategy is especially effective for those who need a sizable loan amount but are stuck at a high rate due to their own credit history.

Hidden Fees and Their Impact on APR

While many lenders advertise “no origination fee,” the reality is that some add hidden costs. These fees inflate the APR even if the nominal interest rate appears low. A loan with a 10% nominal rate but a $500 origination fee can push the effective APR to nearly 12%.

When comparing offers, always check the Annual Percentage Rate (APR) rather than just the stated interest rate. The APR accounts for all fees and gives you a true cost of borrowing.

How to Spot a Good Deal

- Look at the APR, not just the rate.

- Read the fine print for hidden charges.

- Ask about pre‑payment penalties; some lenders charge if you pay off early.

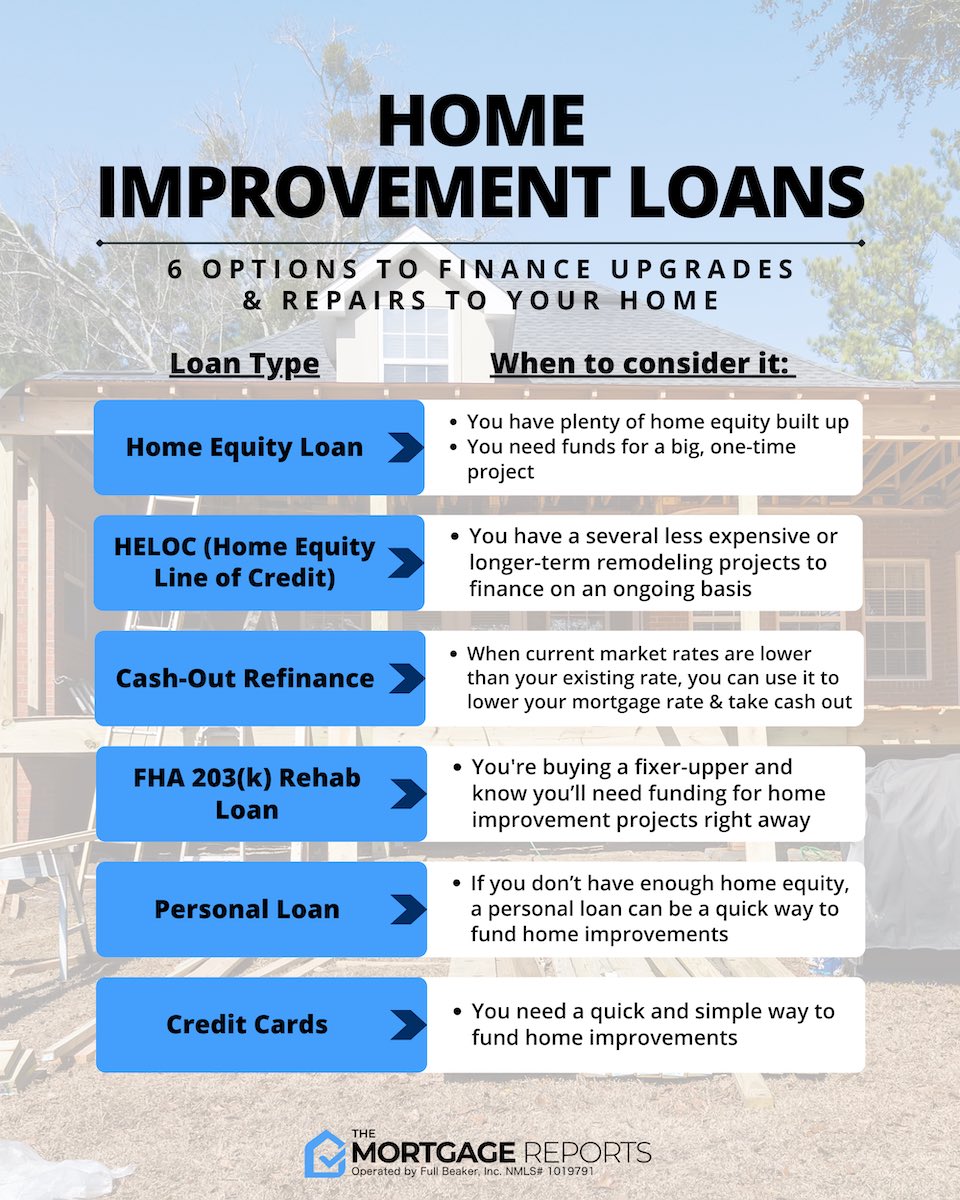

Financing Home Improvement Projects: The Smart Path Forward

Homeowners often turn to personal loans to finance renovations—whether it’s a new kitchen, energy‑efficient windows, or a full remodel. Personal loans offer fixed rates and predictable payments, which can be preferable to variable‑rate credit cards.

However, the cost of borrowing must be weighed against potential return on investment (ROI). A 15% APR loan used for a $10,000 kitchen upgrade might not yield enough savings in energy bills or resale value to justify the expense. Conducting a quick ROI calculation can help determine whether it’s worth taking on debt.

Alternative Financing Options

- Home Equity Lines of Credit (HELOCs): Often lower APRs but require collateral.

- Credit Cards with 0% Intro APR: Good for short‑term needs; watch out for the high post‑intro rate.

- Manufacturer Financing: Some appliance retailers offer promotional rates, but terms can be restrictive.

Choosing the right vehicle depends on your credit profile, the loan amount, and how long you plan to carry the debt. For many, a personal loan remains the most straightforward option—especially when paired with a reputable lender that offers transparent terms.

How Jetzloan Helps You Navigate These Options

If you’re ready to explore personal loans for home improvement or other needs, Jetzloan offers a quick pre‑qualification process that lets you see potential rates and terms without hard credit pulls. Their platform aggregates offers from multiple lenders, giving you a side‑by‑side comparison to identify the best fit for your financial situation.

With Jetzloan’s streamlined interface, you can compare APRs, loan amounts, repayment periods, and even read borrower reviews—all in one place. This transparency helps borrowers avoid hidden fees and make informed decisions that align with their long‑term goals.

What You’ll Get From the Pre‑Qualification

- Estimated APR range based on your credit score.

- Potential loan amounts up to $30,000 (varies by lender).

- Repayment terms from 12 to 60 months.

Once you receive the pre‑qualification snapshot, you can choose to proceed with a formal application or refine your credit profile—perhaps by paying down debt or correcting errors on your report—to secure an even better rate.

Regulatory Landscape and Its Effect on Rates

The Consumer Financial Protection Bureau (CFPB) has intensified scrutiny over loan practices, especially regarding high‑fee structures. In 2026, the CFPB issued new guidelines that require lenders to disclose the total cost of borrowing in a single, easy‑to‑read format. Compliance costs are borne by lenders and passed on to borrowers, partly explaining why APRs remain elevated.

For those who want to stay ahead, it’s wise to keep an eye on upcoming regulatory changes—especially around interest rate caps for specific loan types—which could alter the cost landscape in 2027 or beyond.

How to Stay Informed

- Subscribe to industry newsletters from NerdWallet and CFPB.

- Use credit monitoring services to spot changes in your score that could affect rates.

- Regularly review lender disclosures for any fee adjustments.

The Bottom Line: Timing Is Key

Personal loan rates are a moving target, influenced by macroeconomic trends, regulatory shifts, and individual borrower profiles. While the current environment offers lower rates than the early 2020s, it remains prudent to shop around—especially if you’re planning large expenditures.

For home improvement projects, pairing a well‑structured personal loan with a clear ROI calculation can turn an expensive renovation into a smart investment. And when you’re ready to apply, platforms like Jetzloan provide the transparency and speed needed to make an informed choice without hidden surprises.

Final Thought

Borrowing is more than just a number; it’s a financial decision that can shape your future. By understanding how rates are set, comparing lenders, and staying alert to regulatory changes, you position yourself for the best possible outcome—whether that means upgrading your kitchen or consolidating debt.